In 2024, the most recent FAA reauthorization was signed into law, which allocated $105.5 billion for FAA programs through Fiscal Year 2028. The legislation increases AIP funding to $4 billion per year beginning in FY25, a bump from the $3.35 billion per year that had been in place since FY12. AIP provides grants to airports for projects such as airfield and airport access improvements and capacity enhancements. Funding for AIP grants flows from the Airport & Airway Trust Fund (AATF), which receives revenues from various excise taxes imposed on users of the airport system, including the ticket tax of 7.5% on all domestic travel and a flight segment tax of $5.20 in 2025, $22.20 for international segments, and $11.10 for Alaska and Hawaii. However, as airlines have implemented à la carte pricing, ticket price revenue has suffered because the 7.5% tax is not applied to baggage fees, food sales, or other discretionary passenger purchases. If $4.9 billion in baggage fees collected by airlines in 2018 had been subject to the tax, excise tax revenues would have been about $367 million higher that year alone.

In 2024, the most recent FAA reauthorization was signed into law, which allocated $105.5 billion for FAA programs through Fiscal Year 2028. The legislation increases AIP funding to $4 billion per year beginning in FY25, a bump from the $3.35 billion per year that had been in place since FY12. AIP provides grants to airports for projects such as airfield and airport access improvements and capacity enhancements. Funding for AIP grants flows from the Airport & Airway Trust Fund (AATF), which receives revenues from various excise taxes imposed on users of the airport system, including the ticket tax of 7.5% on all domestic travel and a flight segment tax of $5.20 in 2025, $22.20 for international segments, and $11.10 for Alaska and Hawaii. However, as airlines have implemented à la carte pricing, ticket price revenue has suffered because the 7.5% tax is not applied to baggage fees, food sales, or other discretionary passenger purchases. If $4.9 billion in baggage fees collected by airlines in 2018 had been subject to the tax, excise tax revenues would have been about $367 million higher that year alone. The FAA estimates that $67.5 billion in capital development projects are needed between 2025 and 2029. Comprising everything from surface access and terminal safety to security and others, the $67.5 billion total includes approximately 18,100 projects and reflects development needs for 3,287 existing airports and five new airports.15 Development needs for an airport are based on eligible and justified projects consistent with the airport’s role in the national airport system. ASCE’s Bridging the Gap economic study projected a need of $310 billion between 2024 and 2033, with projected funding from all sources at $168 billion if IIJA investment levels continue from 2026. That leaves a funding gap of $114 billion, or $162 billion if federal investments snap back to prior levels that year.

The FAA estimates that $67.5 billion in capital development projects are needed between 2025 and 2029. Comprising everything from surface access and terminal safety to security and others, the $67.5 billion total includes approximately 18,100 projects and reflects development needs for 3,287 existing airports and five new airports.15 Development needs for an airport are based on eligible and justified projects consistent with the airport’s role in the national airport system. ASCE’s Bridging the Gap economic study projected a need of $310 billion between 2024 and 2033, with projected funding from all sources at $168 billion if IIJA investment levels continue from 2026. That leaves a funding gap of $114 billion, or $162 billion if federal investments snap back to prior levels that year.

Georgia, Inland Waterways, National Category

Startup Uses Drone for Cleaning Water, Collecting Data

U.S. domestic air passenger enplanements increased steadily throughout the last decade, from 629.5 million in 2010 to 811.4 million in 2019. Following the COVID-19 pandemic, air travel has fully recovered to 819.5 million in 2023 and continues to increase. Passenger traffic is forecasted to grow 58% to 1.28 billion annual passengers by 2040. The pandemic did not impact air cargo, and 2021 saw the most cargo in history, with 125.3 million metric tons carried. Funding from the 2021 Infrastructure Investment and Jobs Act (IIJA), which provided $25 billion over five years, and local investments are enhancing passenger experience, especially at larger airports. Still, delays continue to be a major problem because of ongoing workforce and modernization challenges. Although modest funding increases in the latest Federal Aviation Administration (FAA) reauthorization is a positive step, the continued failure to raise the cap on the Passenger Facility Charge represents a missed opportunity, because the projected funding gap is $114 billion over the next 10 years and additional resources will be needed to address this deficit.

that air passenger traffic will increase from 811 million passengers in 2023 to

1.3 billion passengers by 2044

face a workforce gap of

3,000 air traffic controllers

that nearly $68 billion is needed between 2025 and 2029 for

capital development projects

In 2019, the U.S. aviation industry contributed 4.9% to the U.S. Gross Domestic Product (GDP) and generated $1.9 trillion in total economic activity, supporting 10 million American workers. At the state level, impacts vary by population, number of airports, aviation manufacturing, tourism, and other aviation-related business activities. In 2020, the pandemic resulted in a significant decrease in the number of passengers at U.S. airports, while overall economic activity and jobs supported saw similar declines, averaging 50% of the previous year’s numbers.

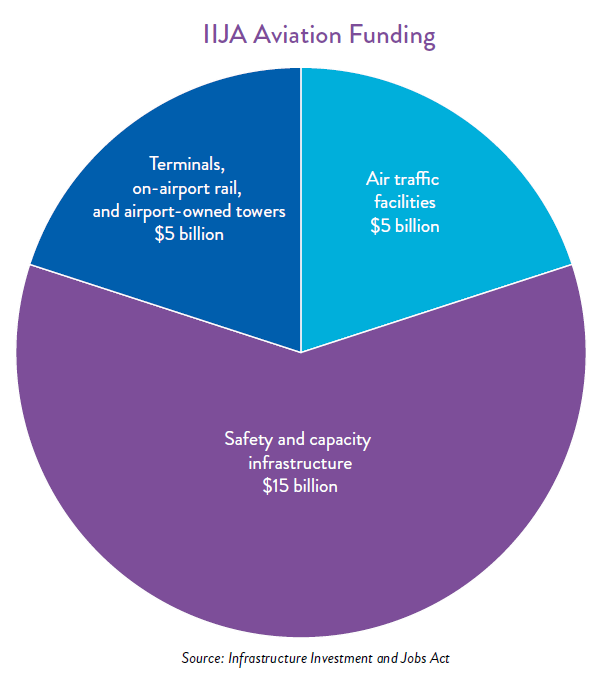

Commercial airports are traditionally supported by four sources of funding: airport-generated revenue; general obligation bonds; federal, state, and local grants, which include the Airport Improvement Program (AIP); and Passenger Facility Charges (PFCs). The IIJA provided $25 billion in additional aviation infrastructure investments. This includes $5 billion for air traffic facilities, $15 billion for airport infrastructure to increase safety and expand capacity, and $5 billion for airport terminals, on-airport rail, and airport-owned towers.

Airports must meet minimum maintenance and operational standards prescribed by federal, state, and local agencies. For instance, the FAA aims for 93% of NPIAS runway pavements to be in excellent, good, or fair condition. In FY23 97.7% of runways at NPIAS airports are rated excellent, good, or fair, but note that a runway in “poor” condition is still safe for flight operations. It simply requires more frequent inspections and often more intensive pavement maintenance.

Airports are a critical component to the movement of goods and people and must be resilient to weather- and human-caused catastrophic events. In addition, airports often serve as a lifeline for urgent relief supplies during emergencies.

Technological advances play a critical role in improving airport service. However, adjusting to and planning for the ever-changing airport environment is increasingly difficult. To tap into transformative potential, airports understand that it is more than just technology—it is a process centered on people that requires a culture shift and executive-level commitment.

Solutions that Work

Photo Attributions

Select your home state, and we'll let you know about upcoming legislation.

"*" indicates required fields