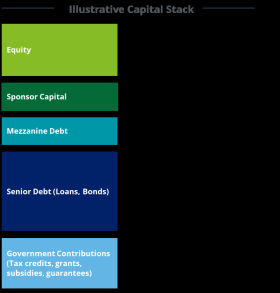

States may consider developing their own loan (senior debt) and grant (government contributions) programs to fund state-specific infrastructure projects. States may develop low-interest loan programs to encourage the construction of infrastructure within their states, which could also attract and leverage other forms of financing from the capital stack through the reduction of project risk having a state government-backed loan with a lower cost of financing. Various states also have state infrastructure banks that provide low-interest loans to borrowers, such as the Georgia Transportation Infrastructure Bank administered by the State Road and Tollway Authority (SRTA).

Infrastructure projects can also consider P3s to help address investment gaps. A P3 is a long-term contractual relationship between a public sponsor (e.g., the government) and a private entity to provide a defined list of services on behalf of the public sponsor. In a P3 arrangement, the public sponsor transfers risks and responsibilities to the private partner in exchange for either a recurring payment (e.g., availability payment for a utility system) or the right to collect revenues from the public (e.g., toll roads or energy user fees). In a P3, the public sponsor retains strategic control over the asset and service delivery. Adoption of a P3 can provide an option for the public sector to accelerate delivery of infrastructure ahead of budgeting cycles and free up limited public resources for other strategic initiatives. Contingent on the structure of the agreement, P3s may also public debt concerns by leveraging private financing (debt, equity) in lieu of traditional public bonds. In certain cases, the contract structure could also include an upfront payment (based on calculations of leveraged efficiencies from the private sector) which provides a public sponsor with a cash influx to address short-term funding gaps for other initiatives and projects. Pennsylvania’s Department of Transportation (PennDOT) developed their Rapid Bridge Replacement program as a P3 and serves as an example of leveraging private sector efficiency. The P3 program repaired 558 bridges in four years, which might have taken more than a decade to repair otherwise.

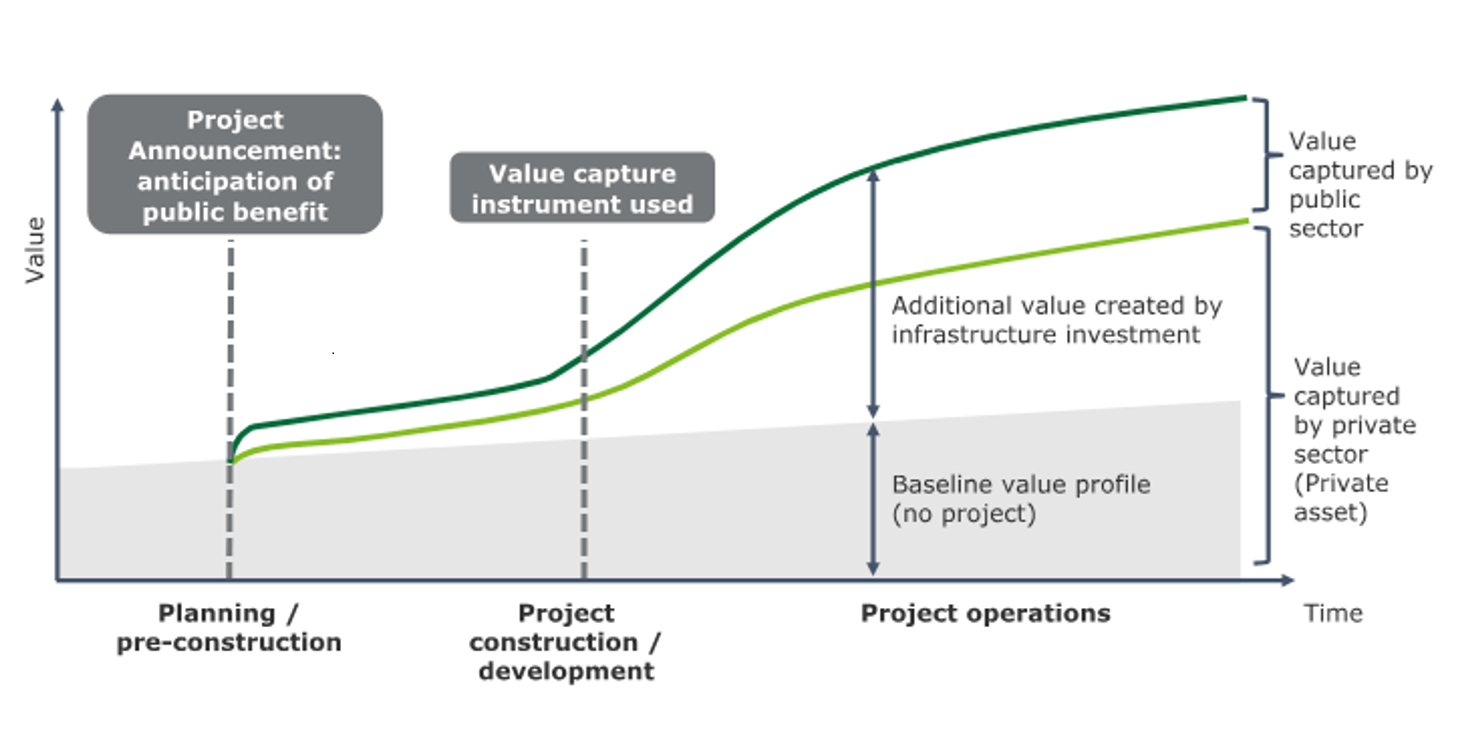

Value capture is another option for financing infrastructure. Value capture is the concept that infrastructure improvements create economic value that both the public and private sectors can “capture” from new infrastructure projects. Typical direct value capture methods transfer economic value from users of the asset/service to the operating entity (user fees, fuel tax, transportation network fees). Indirect value capture methods are financial agreements and mechanisms that allow sponsors to capture future economic value generated indirectly by an asset (tax increment financing, sales taxes, special assessments, etc.). For example, The City of Atlanta (Atlanta) financed multimodal infrastructure improvements by leveraging value capture instruments such as defining a special assessment district and using transportation special-purpose local option sales tax revenues. The figure below highlights the value that new infrastructure projects can create, which can be “captured” and monetized.

In the years to come, diverse funding sources and innovative financing strategies have the potential to play a crucial role in bridging the investment gap and supporting the sustainable and continued development of infrastructure projects across the US. Project developers and government can consider the approaches outlined above to leverage additional funding and financing opportunities in the future. For more information on Deloitte’s Infrastructure advisory services, please visit:

- Infrastructure Advisory Focus Areas and Services | Deloitte US

- Public Infrastructure and Capital Projects Eminence | Deloitte US

This blog contains general information only and Deloitte is not, by means of this blog, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This blog is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this blog.

As used in this blog, “Deloitte” means Deloitte Transactions and Business Analytics LLP, a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of our legal structure. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2025 Deloitte Development LLC. All rights reserved.